jbk_photography/iStock Editorial via Getty Images

Amid elevated market volatility, oftentimes the best way to beat the index movements is to invest in contrarian plays that have little correlation with the broader market. This means digging deep into unloved, forgotten names that may not be the flashiest of the day, but have solid fundamentals against a reasonable valuation.

Surprisingly, one of the names that fits this criteria well is Groupon (NASDAQ:GRPN), the once-popular deals site that has now become quite a niche offering. Shares of Groupon are down more than 20% year to date, but there are surprising fundamental improvements that the company has to call out.

The clouds are clearing up for Groupon

I last wrote a neutral opinion on Groupon last October, when the stock was trading closer to $12 per share. At the time, I had cited green shoots from the company’s ongoing profitability improvements, but I cited concerns over two main things: continued customer losses as well as limited liquidity.

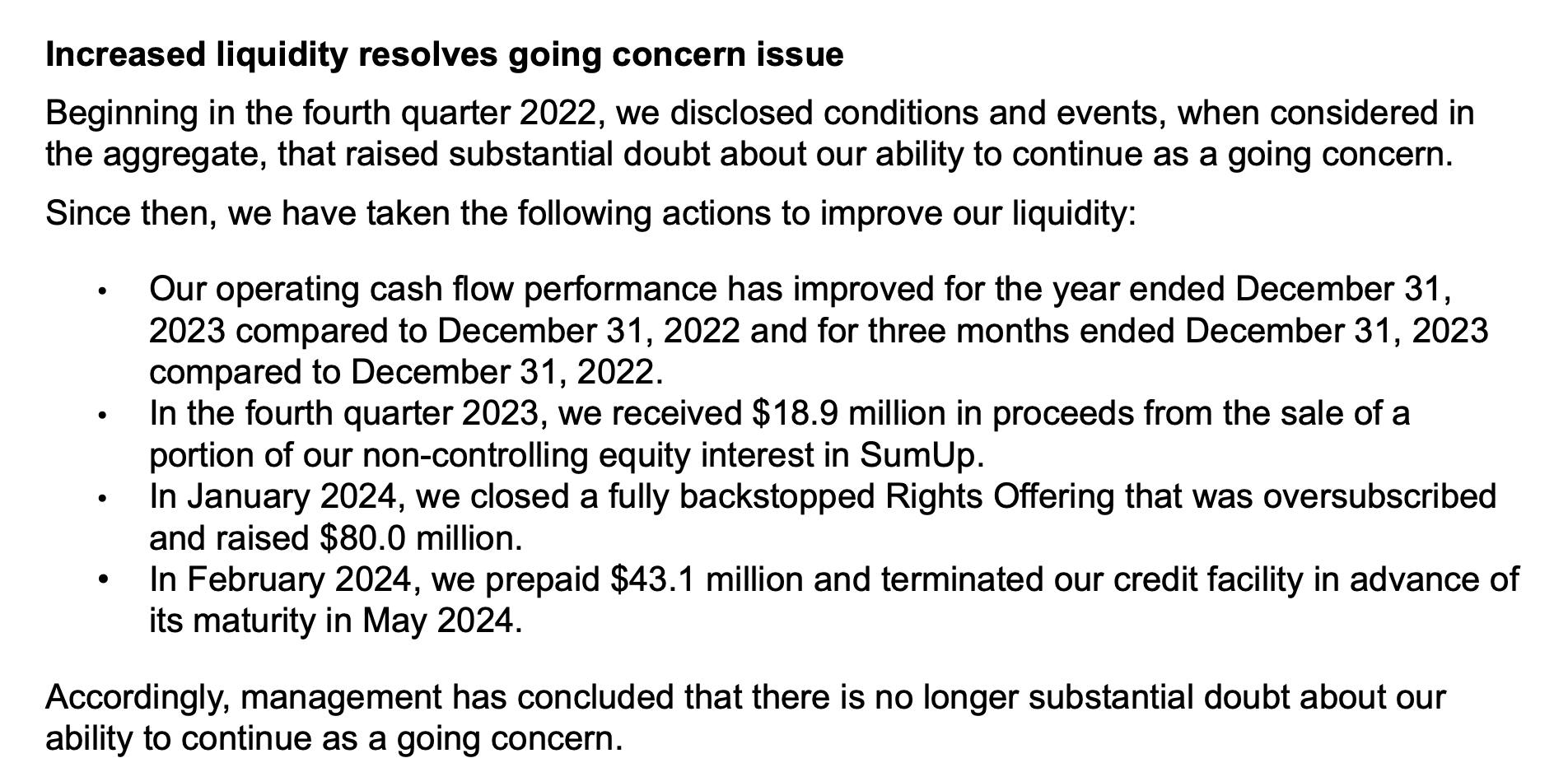

Unfortunately, Groupon continues to see negative y/y comps, but at least revenue declines are moderating (we’ll discuss this more in the next section). However, the company has made notable strides in improving its liquidity position, as shown in its Q4 earnings release statement below:

Groupon liquidity actions (Groupon Q4 earnings deck)

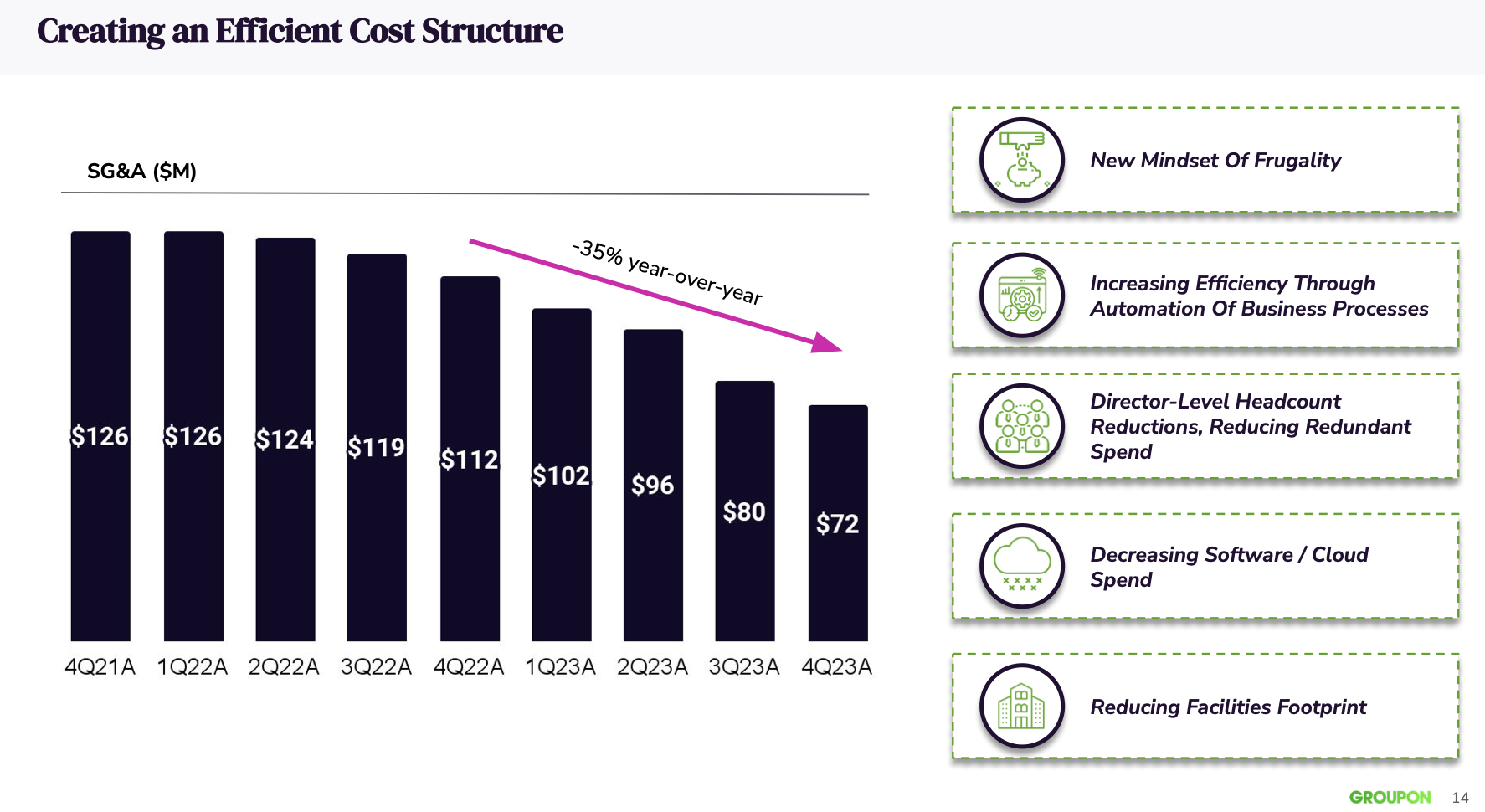

The ongoing operating cash flow improvements are the most important part of Groupon’s improving liquidity position. The company continues to take an aggressive stance toward slicing operating expenses. SG&A costs have fallen every quarter sequentially for the past two years as the company has made middle-management headcount layer eliminations, while also shrinking its real estate footprint.

Groupon SG&A cost trends (Groupon Q4 earnings deck)

As shown in the chart above, Groupon’s SG&A reached a multi-year low of $72 million in the most recent quarter, down -35% y/y. Combined with sales of equity stakes in minority subsidiaries, Groupon ended Q4 with $216.4 million of cash and long-term investments (though it also is burdened with $269.2 million of debt). Full-year FCF in FY23, meanwhile, was -$97 million – so even if Groupon does nothing more to stem its current burn rate (which is unlikely as it continues to slice cost and see moderating revenue declines), it would have more than two years of cash left on its books. Note that Groupon is actually projecting positive FCF this year, with FY23 hopefully being its last full year of FCF burn.

All in all, many of my nearer-term concerns on Groupon have cleared up, and with the sequential improvements to EBITDA that the company is chasing, I am confident enough to be bullish on this stock: it’s worth a small bet in your portfolio. Groupon’s next major catalyst is its Q1 earnings release, expected sometime in mid-June, but I’d recommend locking in a long position now while the stock is in decline.

Q4 download

Let’s now go through Groupon’s latest results in greater detail.

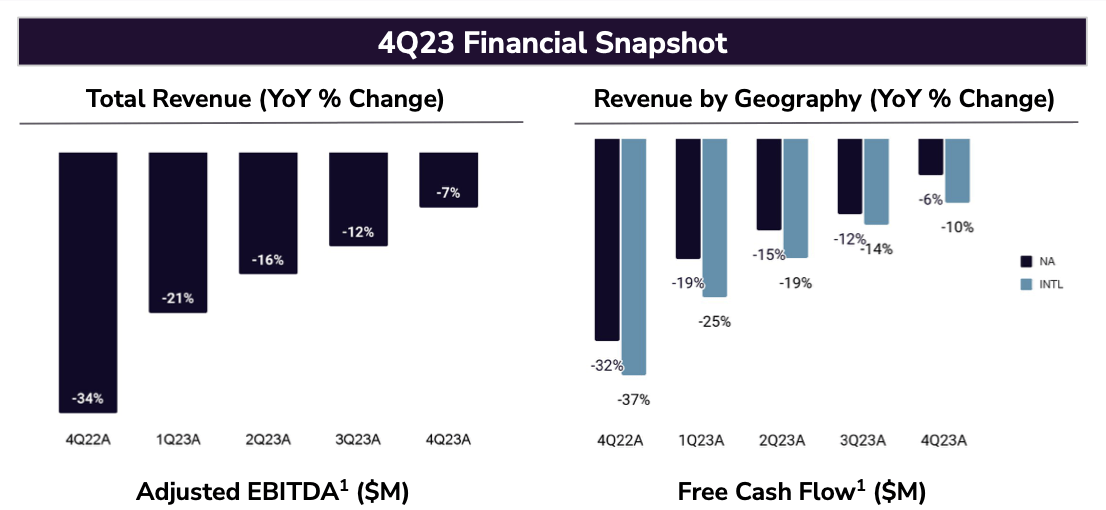

Groupon key trended metrics (Groupon Q4 earnings deck)

The first to note: as shown in the chart above, while Groupon’s revenue continues to decline, comps are getting easier and actual performance is improving. Q4 revenue declined “only” -7% y/y, a five-point improvement versus -12% y/y decline in Q3.

The company noted improving performance during the holiday period, as consumer engagement levels ticked upward through the quarter. Per CEO Dusan Senkypl’s remarks on the Q4 earnings call:

Overall I am pleased with our daily execution during the holiday season as we connected an improved assortment of deals with a performance marketing push and active management of how we distribute our impressions. Our customers responded and we saw uplift in our business and improving trends throughout the quarter.

On the demand side of the marketplace, we saw improving trends in the number of unique visitors visiting our website, driven by growth in paid channels and an improved rate of decline of direct traffic. Within paid channels, we delivered on our desired ROI targets while continuing to grow in SEM and display. And while it is very early, we saw success in our revamped affiliate channels including early traction in the influencer market. Search and relevance continues to be an important priority for us as we improve our algorithm and actively manage the distribution of impressions. Finally, we continue on our initiative to reduce our reliance on promotional spend. As we have discussed before, improving the mix between paid marketing and promotional spend is a key step towards improving the health of our marketplace.

On the supply side of the marketplace, we continue to see strength in our Things To Do vertical and our Enterprise accounts, where we see companies return to our platform after a long hiatus and existing companies increase the amount of business they want to do with Groupon. Both are encouraging signals.”

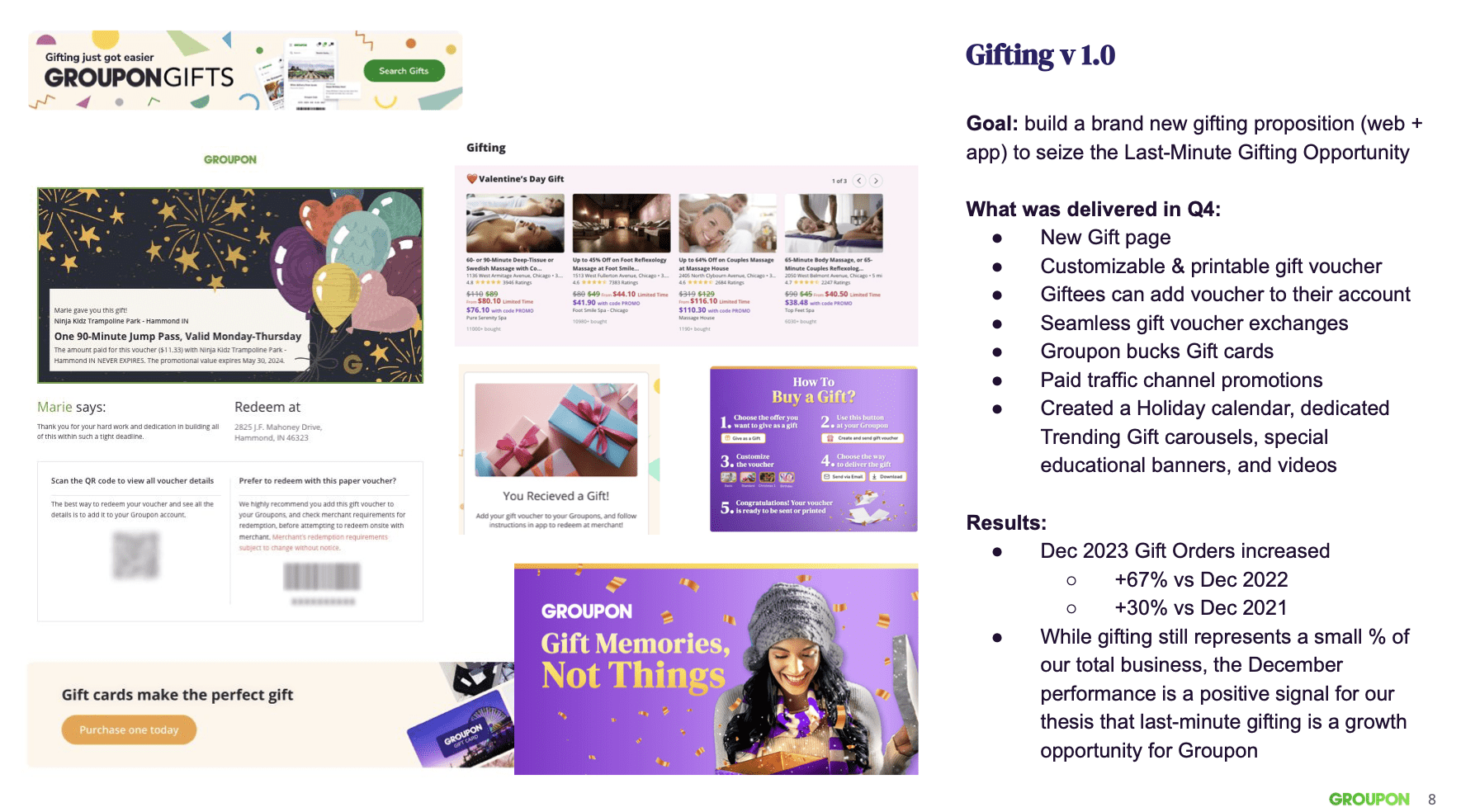

Product innovation is another lever that the company has utilized to drive performance. The company rolled out its gifting feature, with the ability to “gift” somebody an experience. As shown in the chart below, gift orders jumped 67% y/y in the quarter:

Groupon gifting (Groupon Q4 earnings deck)

And from a profitability standpoint, Groupon’s adjusted EBITDA clocked in at $26.9 million in the quarter, versus a loss of -$5.3 million in the year-ago period. EBITDA improved 48% versus Q3 on a nominal basis, while adjusted EBITDA margins of 20% also improved eight points versus Q3.

Valuation, risks and key takeaways

At current share prices just above $10, Groupon has a market cap of $372.6 million; and after we net off the $216.4 million of cash and long-term investments against $269.2 million of debt on the company’s latest balance sheet, its resulting enterprise value is $425.4 million.

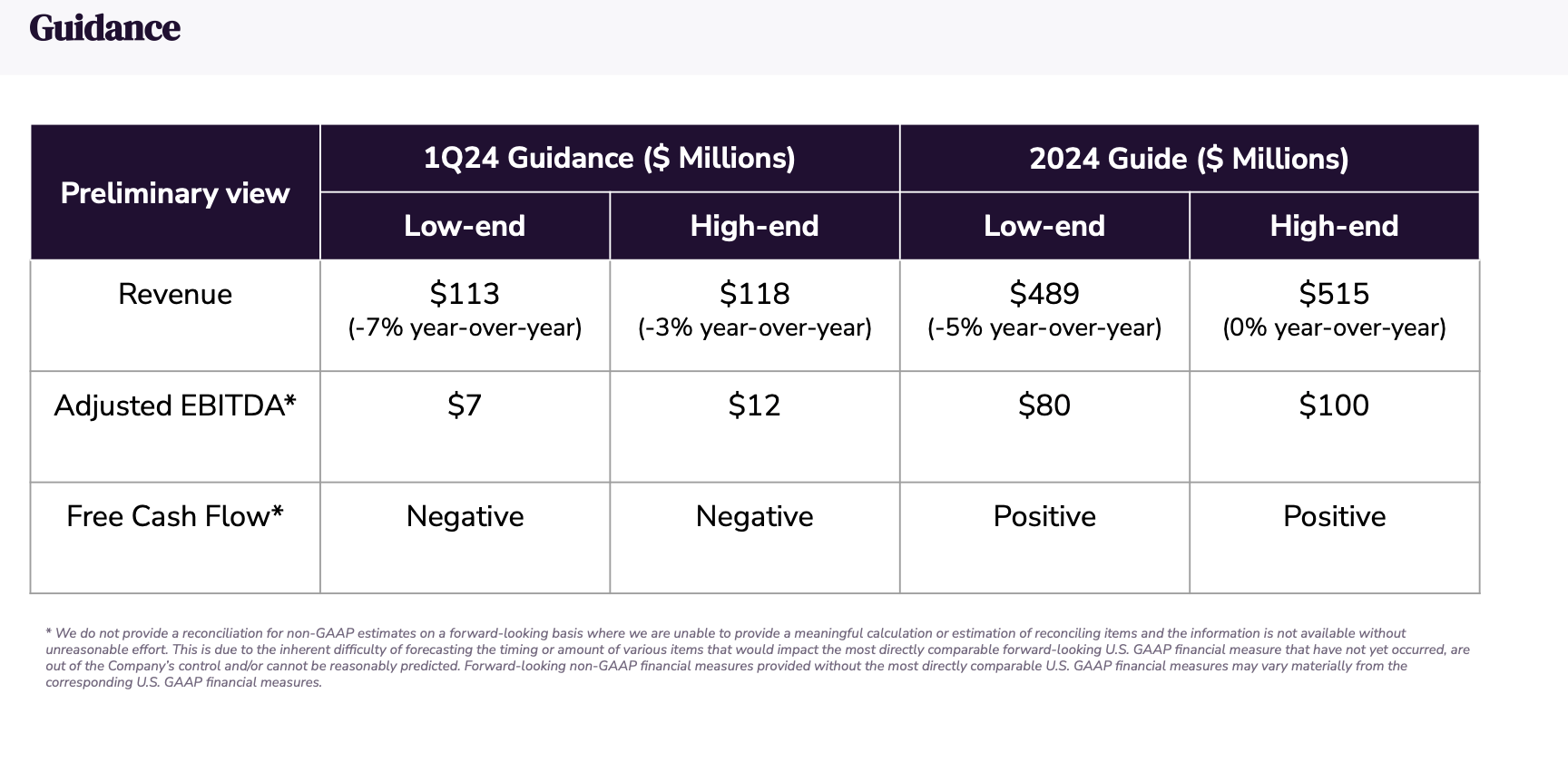

Meanwhile, the company is guiding to an adjusted EBITDA range of $80-$90 million for the year:

Groupon outlook (Groupon Q4 earnings deck)

Considering Groupon exited Q4 at an annualized adjusted EBITDA of over $100 million, and the midpoint margin of ~18% in guidance is lower than 20% in Q4, I’d say this is more than a reasonable outlook. Against this midpoint, Groupon trades at just 4.7x EV/FY24 outlook midpoint adjusted EBITDA.

In my view: Groupon’s outlook skews low. I’m optimistic that the company can hit 20%+ adjusted EBITDA margins in FY24, considering all the cost actions that the company has underway. I’d say the company has the opportunity to hit at least $100 million in adjusted EBITDA, and that it can rally up to 6x EV/FY24 high end adjusted EBITDA of $100 million, which forms my price target of $16 for the company (~40% upside from current levels, and also where Groupon was trading earlier this year before its Q4 results came out).

Of course, Groupon is cheap because there are risks on the horizon. There are two core red flags on my radar. The first is supply growth. Groupon’s ability to continue operating as a provider of niche experiences and deals hinges on its ability to bring these localized offerings to its platform in the first place. With a reduced sales force and headcount overall, Groupon may find it more difficult to source appealing deals to put on its platform. The second is consumer contraction. Groupon’s outlook rests on its ability to perform at roughly flat revenue growth y/y. If supply contraction and general disinterest occur, this may prove difficult to hit.

This being said, I think that comps are easing for Groupon and that at its low, too-cheap-to-ignore valuation, there is more potential reward than risk. It’s time to be bullish here.